1. Executive Summary

This report provides a structured analysis of the Security Information and Event Management (SIEM) market, focusing on vendor positioning, architectural trends, and enterprise selection criteria.

The analysis is based on a review of:

– Industry research (Gartner, IDC, market reports)

– Vendor capabilities and product architectures

– Observed enterprise adoption patterns

Findings indicate that SIEM is evolving from a standalone log management system to a central component within integrated security operations platforms.

At the same time, organizations are increasingly constrained by:

– Rising ingestion and operational costs

– Complex multi tool integration requirements

– Alert fatigue and limited analyst efficiency

– Rapid expansion of cloud and hybrid infrastructures

Industry studies confirm that SIEM deployments often generate high alert volumes and require significant manual effort, reducing analyst efficiency and increasing operational burden.

These factors are driving a market-wide shift toward platform-based security architectures, where SIEM capabilities are embedded within broader, unified solutions.

2. Market Overview & Key Trends (Adjusted Tone)

2.1 Market Reality

Market analysis indicates steady growth in the SIEM segment, with global revenues projected to exceed $20 billion by 2031, driven by increasing cybersecurity threats and regulatory requirements.

However, despite this growth, several structural limitations persist:

– Increasing data ingestion does not consistently translate into improved detection outcomes

– SIEM deployments often require significant tuning and ongoing maintenance

– Detection coverage gaps remain common across enterprise environments

Research highlights that many organizations struggle with data overload, manual workflows, and high operational costs, reducing overall effectiveness of SIEM tools.

This suggests that market growth is occurring alongside operational inefficiencies, creating a gap between platform capability and real-world effectiveness.

2.2 Key Market Trends

Trend 1: Shift Toward SIEM as an Analytics Layer

Industry research indicates that SIEM is increasingly positioned as a data and analytics layer within a broader SOC architecture, rather than a standalone control point.

Trend 2: Cost Optimization as a Primary Driver

Analysis shows that volumetric pricing models are creating cost challenges across large-scale deployments:

– Data volumes are increasing significantly year over year

– SIEM platforms scale cost directly with ingestion volume

Studies confirm that volume-based pricing leads to escalating costs as telemetry grows, making traditional SIEM economics difficult to sustain.

Gartner highlights that traditional SIEM cost structures are becoming difficult to sustain without architectural changes.

Trend 3: Convergence of Security Technologies

The boundary between SIEM, XDR, and SOAR continues to blur. Evidence suggests that organizations adopting integrated detection and response capabilities:

– Achieve faster incident response times

– Reduce operational overhead

– Improve security visibility

This convergence enables faster response times, reduced manual effort, and improved visibility.

3. Research Methodology

This market study is based on a structured evaluation framework designed to ensure objective, consistent, and comparable analysis across leading SIEM vendors.

Research Inputs

The analysis incorporates multiple data sources, including:

– Industry analyst research (e.g., Gartner, IDC, market intelligence reports)

– Vendor product documentation and publicly available materials

– Market growth and adoption data

– Observed enterprise security operations trends and use cases

These inputs were used to assess both technical capabilities and operational effectiveness in real-world SOC environments.

Study Limitations

To maintain transparency, several considerations should be noted:

- Vendor capabilities evolve continuously through product updates and acquisitions

- Scoring reflects publicly available information and observed market positioning at the time of analysis

- Enterprise requirements vary significantly by industry, regulatory obligations, and security maturity

- Individual deployment outcomes may differ based on architecture, staffing, and operational processes

These factors should be considered when interpreting comparative results.

Evaluation Framework

Vendors were assessed across six weighted criteria aligned with enterprise SIEM selection drivers:

1. Total Cost of Ownership (TCO)

2. Detection & Analytics Capability

3. Integration & Ecosystem Coverage

4. Operational Complexity

5. Automation & Response (SOAR)

6. Architectural Approach

Each criterion reflects a critical dimension of SIEM performance based on current market conditions, including increasing data volumes, resource constraints, and security complexity.

Scoring Methodology

– Each vendor was scored on a scale of 1 (Low) to 5 (High) for each criterion

– Scores reflect a combination of:

– Capability maturity

– Operational impact

– Alignment with enterprise requirements

– Criteria were then weighted based on relative importance in modern SIEM selection

This approach ensures that the final evaluation reflects real-world applicability, not just feature availability.

Study Objective

The objective of this methodology is not to identify a “feature rich” solution, but to evaluate: Which SIEM approach most effectively enables efficient, scalable, and integrated security operations.

This distinction is critical, as enterprise priorities have shifted from feature depth to operational performance and architectural efficiency.

4. Competitive Landscape Analysis

4.1 Vendor Comparison Framework

To ensure consistency, vendors were evaluated based on six criteria derived from industry best practices:

– Cost efficiency (TCO)

– Analytics capability

– Integration model

– Operational complexity

– Automation capability

– Architectural approach

4.2 Comparative Analysis of Leading SIEM Vendors

The following table summarizes the findings:

| Vendor | Key Observations |

| Splunk (Cisco) | Delivers strong analytics capabilities; however, operational complexity and cost scaling are consistently cited as challenges in large environments |

| Microsoft Sentinel | Provides deep integration within the Microsoft ecosystem, though dependency on ecosystem and cost variability remain considerations |

| Google Chronicle | Offers high performance analytics and scalability; ecosystem maturity continues to evolve |

| Elastic Security | Enables high customization and flexibility, but requires significant engineering effort for deployment and maintenance |

| IBM QRadar | Maintains a strong position in compliance focused deployments, though innovation pace is comparatively slower |

| Fortinet (FortiSIEM) | Combines SIEM analytics, built-in automation (SOAR), and asset visibility within a unified platform, reducing dependency on external tools and simplifying operational workflows |

4.3 Key Analytical Finding: Integration vs Fragmentation

A comparative analysis across vendors reveals a consistent pattern:

– Vendors with tool centric architectures typically require:

– Multiple additional platforms (SOAR, TIP, asset systems)

– Extensive integration effort

– Vendors with platform centric architectures provide:

– Built-in automation

– Cross domain visibility

– Reduced operational dependency on external tools

4.4 Implication of Architectural Differences

The architectural approach has direct impact on:

| Dimension | Tool-Based SIEM | Integrated Platform |

| Cost | Higher due to multiple tools | Lower due to consolidation |

| Complexity | High (integration heavy) | Reduced |

| Response Time | Slower (disconnected workflows) | Faster (unified workflows) |

| Analyst Efficiency | Lower | Higher |

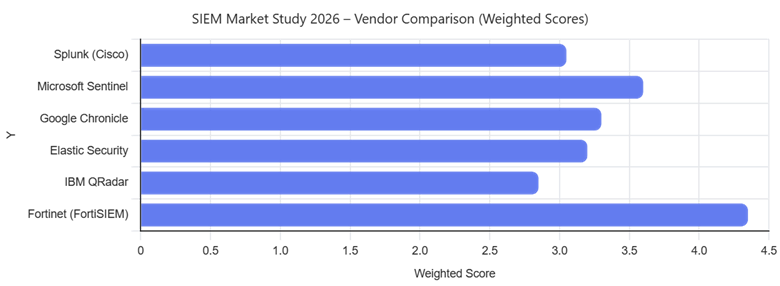

4.5 Quantitative Vendor Scoring Model

To support the comparative analysis, a weighted scoring model was applied across all evaluated SIEM vendors.

Scoring Criteria and Weights

| Criteria | Weight | Description |

| Total Cost of Ownership (TCO) | 20% | Includes ingestion cost, infrastructure, and operational overhead |

| Detection & Analytics Capability | 20% | Depth of analytics, correlation, and threat detection |

| Integration & Ecosystem Coverage | 20% | Ability to integrate across network, endpoint, cloud, and identity |

| Operational Complexity | 15% | Ease of deployment, maintenance, and tuning |

| Automation & Response (SOAR) | 15% | Native automation and response capabilities |

| Architectural Approach | 10% | Degree of platform consolidation vs tool fragmentation |

Vendor Scoring (1–5 Scale)

Platform centric SIEM architectures demonstrate higher overall performance across cost, efficiency, and operational impact.

Key Observations from Scoring Model

The scoring model highlights several important trends:

1. Cost Efficiency is a Differentiator

Platforms heavily reliant on ingestion-based pricing models score lower in total cost efficiency due to scalability challenges.

2. Analytics Capability is Relatively Mature Across Vendors

Most leading vendors deliver strong analytics, resulting in relatively similar scores across this dimension.

3. Integration and Architecture Create the Largest Performance Gap

The largest score variance appears in:

– Integration capability

– Architectural approach

Solutions with native integration across multiple domains and reduced dependency on third-party tools score significantly higher.

4. Built-in Automation Increases Operational Effectiveness

Vendors with embedded SOAR capabilities demonstrate higher overall scores due to:

– Faster response times

– Reduced manual workload

– Improved SOC efficiency

5. Platform-Based Architectures Outperform Tool-Based Models

The highest scoring solutions are those that:

– Combine SIEM, automation, and multi-domain visibility

– Reduce integration complexity

– Enable end-to-end workflows within a single platform

Analytical Conclusion from Scoring Model

The quantitative evaluation indicates that:

- SIEM platforms that provide integrated, multi-function security capabilities within a unified architecture consistently outperform solutions that rely on multiple external tools.

This advantage is most visible in:

– Total cost of ownership

– Operational efficiency

– Speed of detection and response

Interpretation for Enterprise Buyers

From an enterprise perspective, the scoring model suggests that SIEM selection should be based on overall operational impact rather than isolated feature strength.

Additional evaluation criteria may include:

- Existing technology investments and ecosystem alignment

- Internal security staffing and expertise levels

- Regulatory and compliance requirements

- Cloud adoption strategy

- Long-term operational sustainability

Organizations should evaluate SIEM solutions based on their ability to support both current requirements and future security transformation initiatives.

5. Market Reality Check

Analysis indicates that no single vendor leads across all individual technical dimensions.

However, differences become more pronounced when evaluated across end-to-end operational effectiveness.

In particular:

– High analytics platforms introduce complexity and cost challenges

– Open platforms introduce flexibility but require engineering investment

– Cloud native platforms introduce scalability but may increase dependency

In contrast:

– Platforms that combine analytics, automation, and multi domain visibility within a single architecture demonstrate advantages in operational efficiency and cost predictability

6. Future Outlook

The SIEM market is expected to continue evolving beyond traditional log collection and correlation capabilities. Several developments are likely to shape enterprise security operations over the coming years:

- Increased adoption of AI assisted threat detection and investigation

- Greater convergence between SIEM, XDR, SOAR, and exposure management platforms

- Continued pressure on organizations to reduce security tool sprawl

- Growing demand for unified visibility across cloud, endpoint, network, identity, and OT environments

- Increased focus on measurable SOC efficiency and return on security investments

As organizations mature their cybersecurity programs, platform consolidation is expected to become a key strategic objective, influencing future SIEM purchasing decisions.

6. Conclusion

The market analysis demonstrates that SIEM is no longer evaluated solely as a log management or detection platform. Instead, organizations are increasingly assessing solutions based on their ability to support integrated security operations, streamline workflows, reduce operational complexity, and improve overall security effectiveness.

As cybersecurity environments continue to expand in scale and complexity, enterprise priorities have shifted beyond feature depth toward outcomes such as:

- Operational efficiency

- Architectural simplicity

- Integration across the security stack

- Total cost of ownership

In this context, platforms that combine visibility, analytics, automation, and operational efficiency within a unified architecture are becoming more closely aligned with enterprise security objectives.

The findings indicate a clear market shift:

SIEM solutions that minimize reliance on external tools and provide integrated capabilities across detection, automation, and visibility consistently deliver stronger operational outcomes. These platform-based approaches enable more scalable, efficient, and sustainable security operations, making them increasingly relevant for modern enterprise environments.