Moody’s Downgrades Bahrain Long-Term Credit Rating

Moody’s has recently lowered Bahrain’s long-term issuer rating by two notches to B1, from Ba2, and maintained the “negative” outlook. Before venturing into how this will impact the Bahrain’s economy, we need to understand first what is meant by credit ratings.

A credit rating is an assessment of an entity’s ability to pay its financial obligations. the ability to pay financial obligations is referred to as “creditworthiness.” Credit ratings apply to debt securities like bonds, notes, and other debt instruments (such as certain asset-backed securities) and do not apply to equity securities like common stock. Credit ratings also are assigned to companies and governments.

When making investment decisions, credit ratings and any related rating and industry trend reports can be helpful tools, provided they are used appropriately. Credit ratings may offer an alternative point of view to your own financial analysis or that of your financial adviser.

A downgrade to junk status is associated with high risk. Therefore, high borrowing costs. For governments it means allocating more to debt servicing costs (interest payment). Less money will be available for social grants, investment priorities, creating jobs and ultimately reducing the GDP growth potential of the country. More interest payment also crowds out other critical spending. Social services is an example. This is the main reason why a sovereign has to avoid being downgraded into a junk, or sub-investment grade.

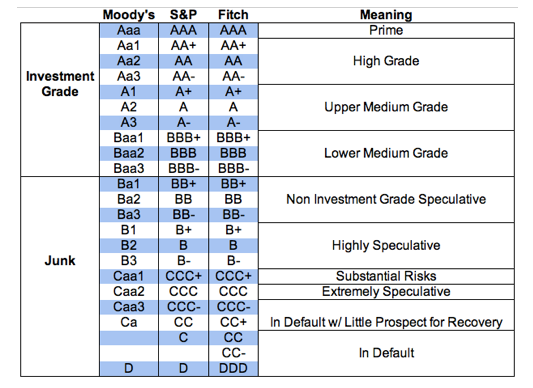

Ratings Agencies Chart

Bahrain was downgraded to junk status by Moody’s back in March 2016 and has been sliding down the scale ever since. With this most recent downgrade it needs to go up four positions before beings considered as investment grade.

The recent downgrade to B1 reflects Moody’s view that the credit profile of the Bahraini government will continue to weaken materially in the coming years. The rating agency expects Bahrain’s government debt burden and debt affordability to weaken further significantly over the coming two to three years.

Although the Bahraini government has taken initial steps towards economic reforms, including lifting some subsidies from fuel and utility tariffs, government restructuring, and increasing fees on government services, these steps are not considered to be aggressive enough in light of the financial challenges. In Moody’s view, the most prominent revenue measure is the introduction of a value-added tax from 2018, but even this measure lacks clarity.

While Moody’s acknowledges the fact that Bahrain’s economy is fairly diversified, with non-oil sectors contributing close to 80% of nominal GDP on average since 2010, it is wary that the government shows no indication that it will use this economic base to materially diversify its revenue base to reduce its reliance on oil-related income which will continue to suffer from weak oil prices in the coming years. Non-oil economic performance will be supported by access to funding under the Gulf Development Fund. While these funds are not part of the Bahraini government’s budget, they will support the government in reducing investment expenditure without unduly harming growth.

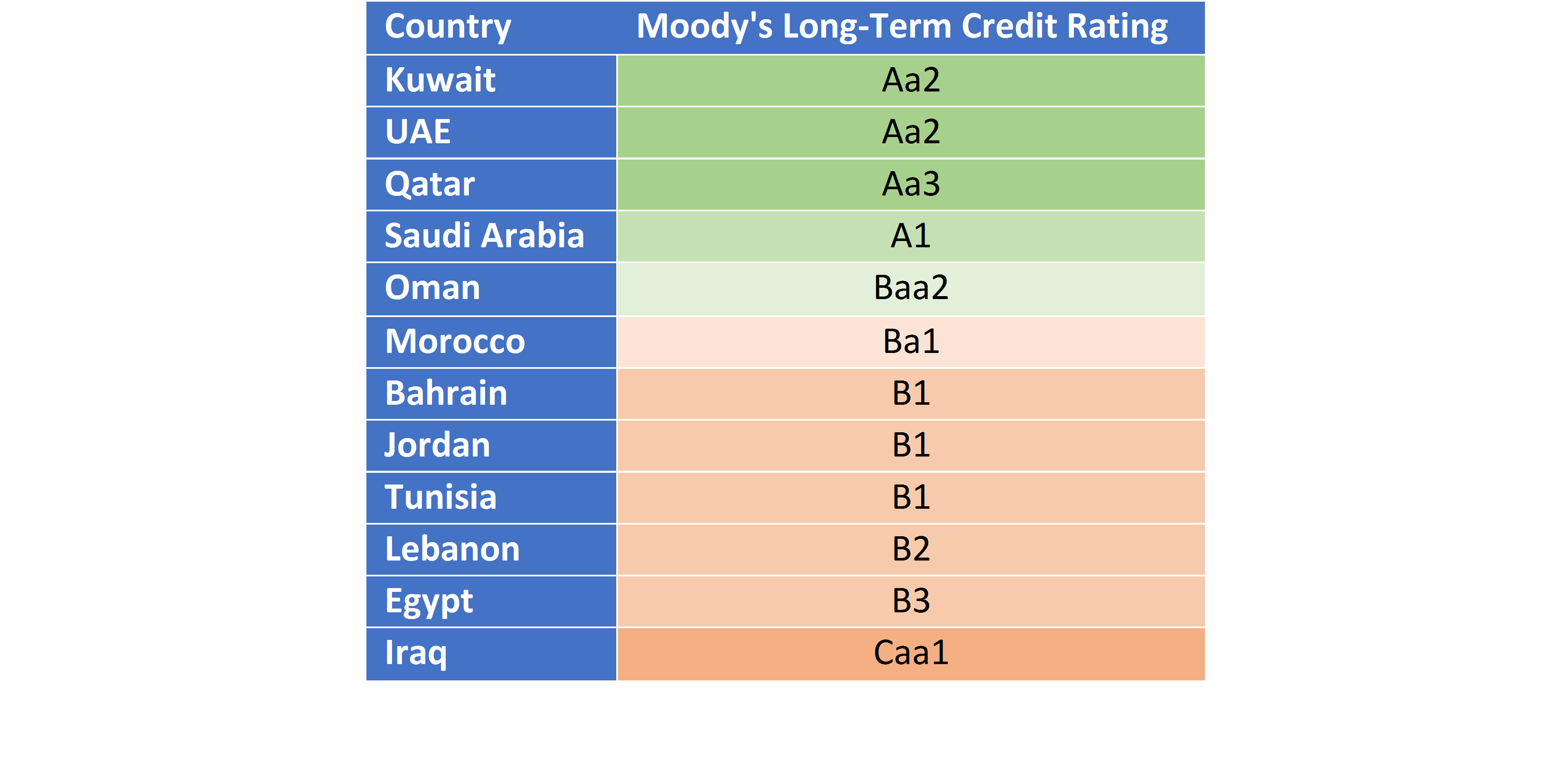

Comparison of Moody’s Rating for Arab Countries

Bahrain’s net asset international investment position, its stock of foreign assets minus foreign liabilities, which stood at 74.5% of GDP in 2016, provides some form of external buffer. However, Moody’s expects it to decline significantly because external liabilities will increase at a much faster rate than the country’s assets. More importantly, foreign exchange reserves at the Central Bank of Bahrain are low and very volatile, covering only around one month of goods and services imports. Following a pause in the dissemination of this data in 2015, the time series disclosed by the central bank more recently shows a material decline in foreign exchange reserves over the last two years, averaging only around $2.5 billion in the first quarter of 2017.

RATIONALE FOR THE NEGATIVE OUTLOOK

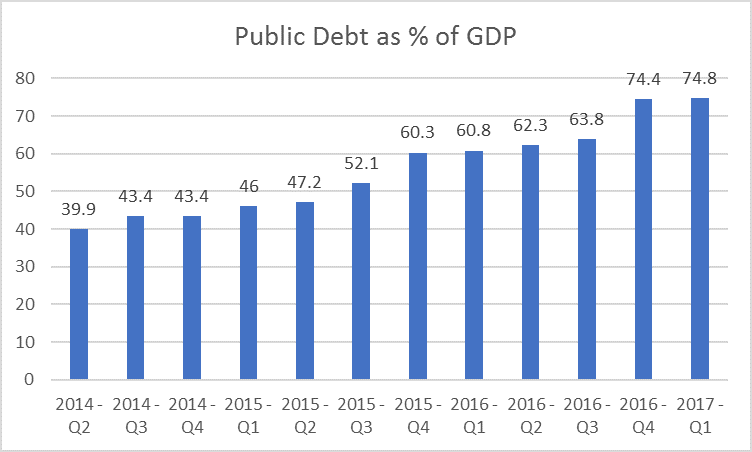

The negative outlook reflects continued downside risks to the B1 rating, which manifest themselves in heightened government and external liquidity risks. Given the expected large fiscal deficits and sizable amortization payments falling due over the coming years, Bahrain’s government gross financing needs will reach more than 30% of GDP over the next two years.

Bahrain Public Debt as Percent of GDP

The further deterioration in the government’s balance sheet, combined with continued external debt issuance from other countries in the region expected in 2017-2018, will lower the supply of external funding. In addition, in light of rising global interest rates the cost of funding will go up.

Moody’s expects that the combination of these two factors heightens the risk that finance is obtainable only at much less affordable rates for Bahrain, or potentially reduced amounts. While Moody’s would expect support from neighboring countries in times of crisis, predominantly from Saudi Arabia, there is no clarity about the form and timeliness of this support in the event that external funding dries up.

WHAT COULD MOVE THE RATING UP/DOWN

Leave a Reply

Want to join the discussion?Feel free to contribute!