Absorption costing vs Variable costing

The success of a manufacturing business primarily depends on the way that the products are costed. There are different kinds of costs involved in a manufacturing organization. Knowledge about the difference between absorption costing and variable costing is essential to do the product costing.

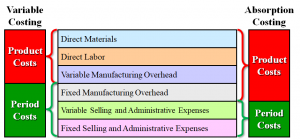

Mainly, the costs can be recognized as variable costs and fixed costs. Absorption costing and variable costing are two different costing methods used by manufacturing business. This difference occurs as absorption costing treats all variable and fixed manufacturing costs as product cost while variable costing treats only the costs that vary with the output as product cost. A business cannot exercise both the approaches at the same time while the two approaches, absorption costing and variable costing, carry their own advantages and disadvantages.

Absorption vs Variable

So, what is variable costing?

Variable costing, known also as direct or marginal costing reflects only the direct costs as the product cost. Therefore, the cost of a product consists of direct labour, direct material and the variable overhead. Fixed manufacturing overhead is considered as a periodic cost like the administrative and selling costs and charged against the periodic income.

Variable costing produces a clear picture on how the cost of a product changes in an incremental manner with the change in level of production of a manufacturer. Nevertheless, since this method does not reflect the overall manufacturing costs in costing its products, it minimises the overall cost of the manufacturer.

What is Absorption Costing?

Absorption costing, known also as full costing or traditional costing, calculate both fixed and variable manufacturing costs into the unit cost of a specific product. Thus, the cost of a product under absorption costing consists of direct material, direct labour, variable manufacturing overhead, and a portion of a fixed manufacturing overhead absorbed using a suitable base.

Some people believe that using absorption costing is the most effective method to calculate the cost of a unit because absorption costing takes all the potential costs into consideration in the calculation of per unit cost. Moreover, using this method allows the inventory to carry a portion of the fixed expenses. By showing a highly valued closing inventory, the profits for the period will be improved. Moreover, this can be used as an accounting trick to reflect higher profits for a certain period by moving fixed manufacturing overhead from the income statement to the balance sheet as closing stocks. The similarity between Absorption Costing and Variable Costing is that the purpose of both approaches are the same; to value the cost of a product.

Leave a Reply

Want to join the discussion?Feel free to contribute!